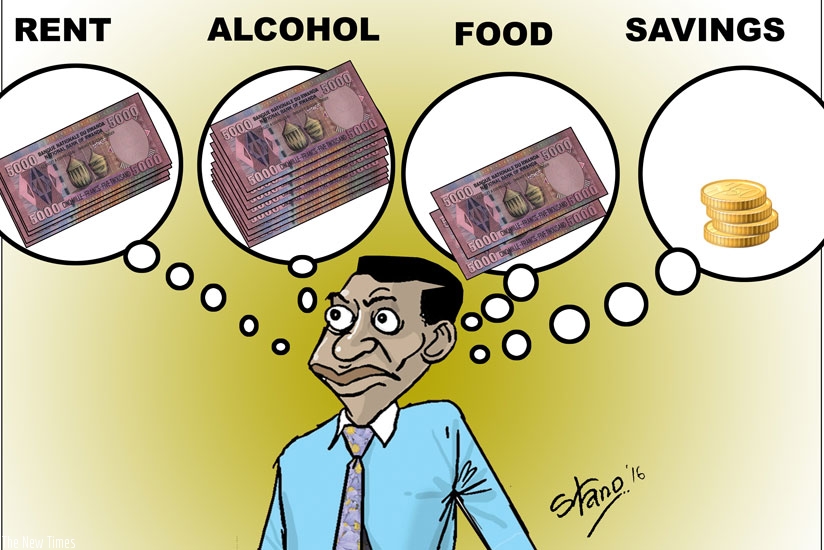

Rwandan youth on how they spend their money

Many years ago, the earnings born of the labor of a young man or woman’s toil went into supporting their families and other rather heavy responsibilities. They paid school fees for their siblings, put food on the table, kept the eviction notice away and secured their own financial future.