Insight

Are you living a borrowed lifestyle?

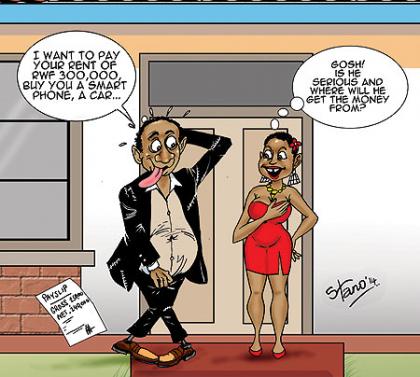

THE 2004 movie Seat Filler may never be listed as a life changing movie or even worthy of an Oscar but it sure does reflect a real life story. The character, Derrick, played by Duane martin, is an ambitious law student trying to stay afloat during hard financial times. In the midst of his ‘hustles’ he falls for a rich pretty musician, Jhnelle, played by Kelly Rowland.

Jhnelle thinks Duane is well off. To fit in this frame, Duane tries all means to keep up appearances and spends over and above his means. Eventually, it drives him to the edge. You may not have watched the movie but we all know a real life “Duane”, or have at least heard of one.

Duane’s story is familiar with many of today’s youth.