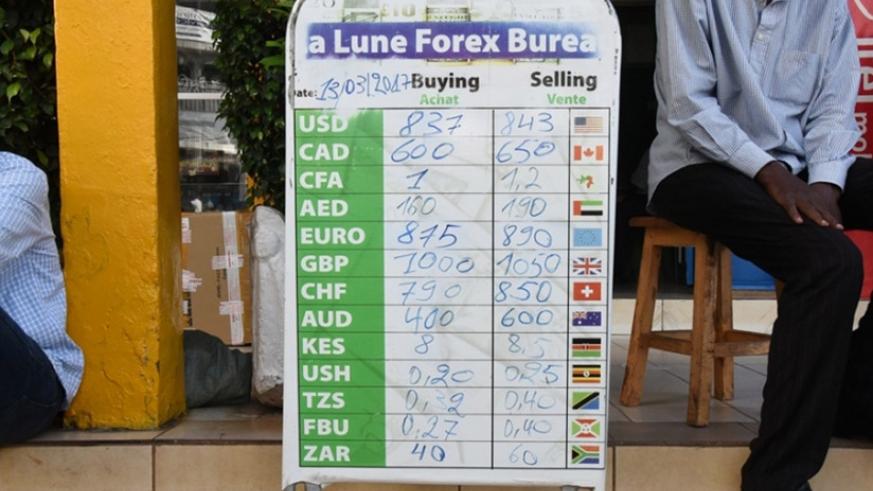

In April 2018 when I first arrived in Rwanda, the franc was trading at Rwf 860 against the US Dollar. In the third week of August, the exchange rate is edging towards Rwf880, which reflects a 2 per cent depreciation of the Rwf against the USD. Over the long term, RWF VS USD in 2002 was 475 and now at 875. This represents 84 per cent of the RWF against the USD. A similar trend is observed in most Africa countries. For example Uganda over the corresponding period has seen its currency depreciate by 114 per cent. Accordingly, Rwanda now runs a flexible exchange rate regime that is fully market driven with intermittent intervention by Central Bank to smoothen volatility and curb speculation. To do that effectively requires adequate foreign exchange reserves – and Rwanda has peripheral levels estimated at 4 months of import value. Persistent depreciation of the franc points to long term structural challenges exhibited by the health of the Balance of Payment (BoP) position. The BoP, which measures external competitiveness, comprises three major accounts: the current, capital and financial. The current account’s major component is the trade balance account (difference between imports and exports). Rwanda runs a trade deficit (10% of GDP in 2017) where imports of goods and services outstrip exports. The imports include a sizeable component of large infrastructure projects. Capital expenditure which accounts for 40 per cent of Rwanda’s national budget significantly raises the import bill. The wider the trade deficit, the more the domestic currency is susceptible. The trade imbalances are arguably central to tension between the US and China. Income sub account of current account relates to foreign investors repatriation against natives income inflows. This mainly refers to incomes from factors of production (rent, wages, interest and profits). This account is also in deficit for Rwanda as is for most developing countries. The last account of current account is the official transfers which include remittances and grants. These have been positive for Rwanda with grants alone accounting for 4 per cent of GDP. Notably remittances are different from income repatriation as they relate to the sum of money sent in payment or as a gift. Overall, the current account deficit for Rwanda has narrowed, reaching 6.8 per cent of GDP in 2017 from over 15 per cent in 2016, in part attributed to the completion of projects like Kigali Convention Centre and the Marriot hotel. However, the deficit for the first half of this year has risen and expected to widen due to the increase in oil prices. In simple terms, the presence of the current account deficit means that demand for foreign currency (for ease we refer to USD) outstrips the supply of the USD and this is what puts pressure on the franc. The deficit also implies that domestic savings being lower than investments and this savings investment gap is what is financed by external sources or met by inflows into the other two accounts of balance of payment(financial and capital account). Financial account relates to direct investment by foreigners also known as FDI against investments by Rwandan natives to the rest of the world, net portfolio investments in stock market and government securities. Lastly, capital account mainly captures the development (public sector) loans for capital investments which are also sizeable (USD 300 million in 2017) and expected to increase as 40 per cent of the public capital projects involve foreign exchange financing in budget for 2018/19. In a nutshell, when the USD deficit in current account is not met by USD inflows financial and capital account, then an unfavorable balance of Payments position (BoP) is resultant. The wider the BoP deficit, the more local currency is likely to be susceptible to depreciation and the gap will likely to be met by draw down of foreign currency reserves or borrowing. The latter is why IMF was started in 1944 to provide BoP lending. While BoP position for Rwanda was favourable in 2017, the expected rise in current account deficit is likely to outstrip the inflows in capital and financial as was the case in 2016 and 2015. The recent spate of depreciation of the franc against the USD and other major trading currencies is indicative of mismatches in balance of payment and remedies are both short to long term. The deficits can spur growth if linked to highly productive areas but also come with accumulation of liabilities in foreign currencies that have to be paid off in future. It is critical that borrowed funds are linked to optimally returning projects. Increased policy focus on promotion of exports as well as increased domestic production of high value products is commendable. Enock Nyorekwa Twinoburyo (PhD) is an Economist.